This article presents a divergent hypothesis from Tyler Cowen's lack of 'low hanging fruit' hypothesis for the current Stagnation (discussed in

my previous post).

I was going to make one quick mention of a pure economics based thought that might have contributed to our current depression but it was based on an understanding inversion (see tiny writing below):

The 1970s switch of Government policy away from Keynesian practises towards monetary policies that buffered the economy from depressions and recessions may have precipitated the financial crisis by their very success: economic fluctuations shake the wastage out of the system, forcing inefficient businesses to shut down, reform or lay off unproductive staff. Keeping things steady just allowed more detritus to accumulate on the buckaroo donkey, saving all the pain for one big, inevitable mess... Well, actually that's complete nonsense!; It was *Keynesianism* that involved strong state intervention (like The New Deal). The 70s and 80s saw the rise of neo-liberalist policies promoting deregulated, free markets and privatisation. So, if anything one would have to blame *over* optimisation for the crash.

+ Introducing Kondratieff waves:

To say that (inter)national economies are complex things is a blatant understatement. Many factors can effect a short term change in GDP growth rate; changes in: money supply, taxation, national interest rate, financial/business regulations (or removal of), public sector redundancies, etcetera. These have each caused quick and apparently large fluctuations in the past, but ultimately such disturbances only manifest for a couple of years at most before return to equilibrium. No amount of fiddling with these factors can stimulate sustained economic growth. Period. Yet on aggregate, since records began, the world GDP has *

always* grown, year on year, even during the great depression, world wars and right now.

|

| US GDP per person - "The Singularity is Near" |

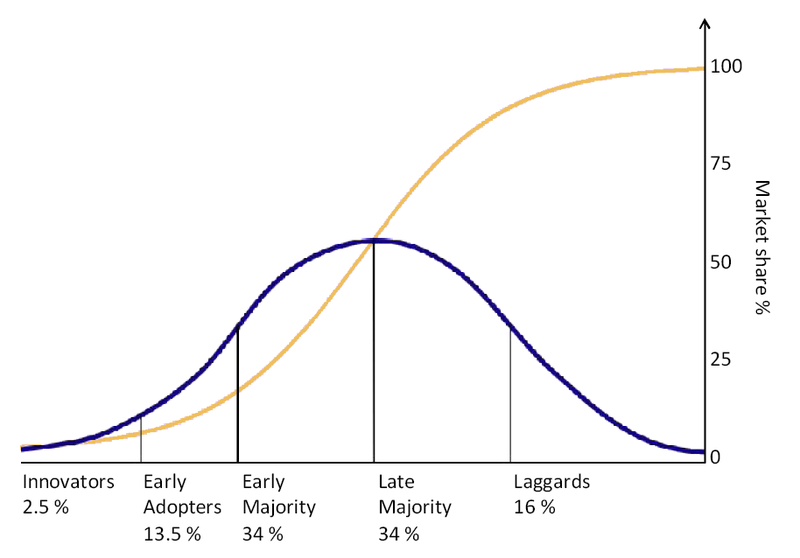

This continual rise in per-person wealth, standard of living and productivity has come from a succession of technological innovations that have permeated society. Although, from an historical distance, the long term growth trend of a country looks pretty smooth, innovation uptake by members of a society tends to following a wave of adoption. Very gradual at first, rapid as it gains widespread popularity, but then perhaps never quite reaching *

everyone*.

There are only a discrete few innovations that are such majorly influential improvements to life as to have become ubiquitous (for example: mains electricity, automobiles, the internet), so they are spaced along our past. Each major innovation stimulated frenzied economic activity, indeed much employment was necessary to build, from nothing, massive infrastructure or industry (e.g. the railway/motorway network, industrial revolution). Lulls occur after each wave of innovation (because science takes time and) because the start of a wave is dependant on the new environment created by the previous one. So one should expect GDP growth history to be a little lumpy; a series of economic revolutions.

Nikolai Kondratieff wrote of his observation of a long wave economic cycle, back in 1925. It earned him Soviet Gulag, death by Stalin, and title to this theory (respectively). He estimated a fixed period of 50-60 years per cycle of: expansion, stagnation, recession. Since then it has been more commonly split into 4 seasons or irruption, frenzy, synergy, maturity (or such like).